What is the Electric Ships Market Overview – definition, scope, and significance?

The Electric Ships Market encompasses vessels that derive propulsion power wholly or partially from electrical energy sources, including battery‑electric, plug‑in hybrid, and conventional hybrid configurations. The scope covers all ship classes—from ferries and cruise liners to military destroyers and aircraft carriers—and spans power ratings from under 75 kW to more than 7 560 kW, as well as operational ranges from less than 50 km to over 1 000 km. Its significance lies in reducing greenhouse‑gas emissions, complying with stricter maritime regulations, and lowering operating costs through higher energy efficiency and lower fuel consumption.

What are the key drivers, restraints, challenges, and opportunities shaping the Electric Ships Market?

Key drivers include tightening IMO carbon limits, increasing public demand for clean transport, and advances in battery density that make electric propulsion viable for larger vessels. Restraints stem from high upfront capital costs, limited charging infrastructure in ports, and the weight penalty of large battery packs. Challenges involve integrating electric systems with legacy ship designs and ensuring safety standards for high‑energy storage. Opportunities arise from government subsidies, green financing, and the emergence of fast‑charging technologies that can shorten turnaround times for ferries and short‑range vessels.

What growth trends are currently influencing the Electric Ships Market?

Current trends feature a rapid shift toward battery‑electric ferries serving short‑haul routes, the adoption of plug‑in hybrid systems for cruise ships to meet intermittent power peaks, and the exploration of hydrogen‑fuel‑cell‑electric hybrids for longer voyages. Manufacturers are also standardizing modular battery packs to accelerate retrofitting, while digital twins are being employed to optimize energy management in real time. These trends collectively accelerate market adoption and broaden the range of ship types eligible for electrification.

How did COVID‑19 impact the Electric Ships Market, and what is the recovery trajectory?

The pandemic caused temporary delays in shipbuilding projects and disrupted supply chains for batteries and power electronics, slowing new orders in 2020‑2021. However, heightened awareness of sustainability and the need for resilient, low‑emission transport accelerated post‑pandemic investments. Recovery is evident in renewed funding for green ports and a surge in procurement of electric ferries for urban mobility, positioning the market on a strong upward trajectory aligned with the projected CAGR of 9.78%.

Who are the major competitors in the Electric Ships Market and how is consolidation evolving?

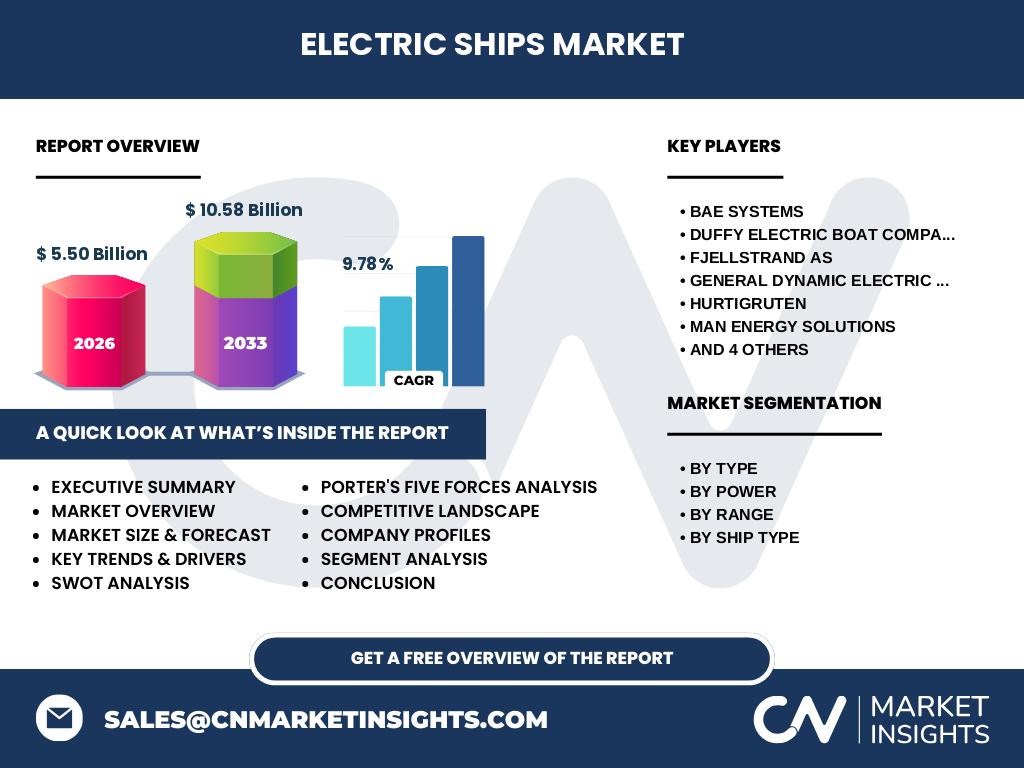

Leading players include BAE Systems, Duffy Electric Boat Company, Fjellstrand AS, General Dynamics Electric Boat, Hurtigruten, MAN Energy Solutions, PortLiner, Siemens Energy, VARD AS, and X‑Shore. Competition centers on battery technology, integrated propulsion systems, and ship‑building expertise. Recent consolidation is modest, with strategic alliances forming between shipyards and energy firms to combine manufacturing capacity with advanced power‑train solutions, thereby enhancing market reach without extensive mergers.

What are the high‑level insights from the Executive Summary of the Electric Ships Market?

The market was valued at USD 5.50 billion in 2026 and is forecast to reach USD 10.58 billion by 2033, reflecting a robust CAGR of 9.78%. Growth is driven by regulatory pressure, technological progress, and expanding port infrastructure. Battery‑electric ships dominate the high‑power segment, while hybrid solutions retain relevance for larger vessels requiring extended range. Geographic demand is strongest in regions with mature maritime networks and supportive policy frameworks, positioning the market for sustained expansion.

What is the forecast for the Electric Ships Market from 2025 to 2032?

Based on the provided CAGR of 9.78%, the market is expected to continue its upward trajectory, nearly doubling from the 2026 baseline of USD 5.50 billion to an estimated USD 10.58 billion by 2033. Annual growth will be driven by increased orders for battery‑electric ferries, hybrid cruise ships, and military vessels adopting electric propulsion to meet emissions targets. The forecast underscores a rapidly expanding opportunity set for suppliers across the value chain.

How is the Electric Ships Market sized and shared across its segmentation?

By type, the market is split among Battery Electric Ships, Plug‑In Hybrid Electric Ships, and Hybrid Electric Ships, each addressing different range and power requirements. Power segmentation ranges from less than 75 kW to more than 7 560 kW, catering to vessels from small fishing boats to large aircraft carriers. Range categories—under 50 km, 50‑100 km, 101‑1 000 km, and over 1 000 km—reflect operational use cases such as harbor shuttles, regional ferries, and long‑haul cargo ships. Ship‑type segmentation includes Cruise Ships, Ferries, Tankers, Bulk Carriers, Fishing Vessels, Destroyers, and Aircraft Carriers, illustrating the market’s applicability across commercial and defense sectors.

What is the global distribution of the Electric Ships Market size and share by region?

The market’s geographic distribution aligns with regions that possess advanced maritime infrastructure and strong regulatory incentives for decarbonization. While specific regional monetary values are not disclosed, the overall market growth is driven by concentrated activity in North America, Europe, and Asia‑Pacific, where port electrification projects and government subsidies are most pronounced. These regions collectively account for the majority of the USD 5.50 billion 2026 market size.

What detailed performance trends are observed in each major region?

In North America, electric ferries dominate short‑range routes, supported by state‑level clean‑transport grants. Europe’s emphasis on stringent IMO compliance and extensive coastal networks fuels hybrid cruise ship projects and extensive port‑charging installations. The Asia‑Pacific region, with its large shipbuilding base, is rapidly adopting battery‑electric solutions for inland waterways and coastal vessels, leveraging economies of scale. Emerging markets are beginning pilot programs, but growth remains modest compared with the three leading regions.

Which companies lead the Electric Ships Market and what are their strategic approaches?

BAE Systems focuses on electric propulsion for naval destroyers and carriers, emphasizing low‑observable technology. Duffy Electric Boat Company specializes in small‑craft battery systems for harbor operations. Fjellstrand AS and VARD AS leverage ship‑building expertise to integrate hybrid modules in commercial vessels. General Dynamics Electric Boat targets submarine and surface combatant electrification. MAN Energy Solutions and Siemens Energy provide integrated power‑train solutions across all power bands. PortLiner and X‑Shore concentrate on modular battery packs and rapid‑charge infrastructure, while Hurtigruten pilots electric cruise itineraries to showcase sustainability.

How does Porter’s Five Forces assessment describe the Electric Ships Market?

Threat of new entrants is moderate; high capital requirements and technical expertise create barriers, yet niche startups can enter via specialized battery modules. Bargaining power of suppliers is relatively high because battery manufacturers are limited and critical to performance. Bargaining power of buyers is growing as ship owners demand cost‑effective, low‑emission solutions. Threat of substitutes remains low; diesel propulsion is the only viable alternative but faces regulatory decline. Industry rivalry is intense, driven by innovation races among established shipyards and energy firms.

What are the SWOT highlights for the Electric Ships Market?

Strengths: Strong regulatory tailwinds, clear environmental benefits, and advancing battery technologies. Weaknesses: High initial CAPEX and limited charging infrastructure. Opportunities: Green financing, government incentives, and emerging fast‑charging standards. Threats: Supply‑chain disruptions for lithium‑ion cells and potential regulatory shifts affecting subsidy levels.

What does the value chain of the Electric Ships Market look like?

The value chain starts with raw material suppliers (lithium, cobalt, aluminum), proceeds to battery cell manufacturers, then to system integrators that assemble power‑train modules. Shipyards incorporate these modules during construction or retrofitting, followed by ship owners operating the vessels. Supporting services include port‑level charging infrastructure, maintenance providers, and software firms delivering energy‑management platforms. Each link adds value through specialization, with strong interdependence between battery technology and ship‑building expertise.

What key investment insights can be drawn for stakeholders in the Electric Ships Market?

Investors should prioritize companies that own end‑to‑end capabilities—especially those coupling battery production with ship‑building. Funding projects that develop port‑charging networks yields both direct returns and indirect market stimulation. Green bonds and sustainability‑linked loans are increasingly available for electrification initiatives, offering attractive risk‑adjusted yields. Finally, diversifying across power‑rating segments mitigates exposure to any single vessel class’s adoption curve.

What conclusions can be drawn about the Electric Ships Market?

The Electric Ships Market is transitioning from niche applications to mainstream adoption, underpinned by a strong regulatory push and rapid technological gains. With a projected market size of USD 10.58 billion by 2033 and a healthy CAGR of 9.78%, the sector presents compelling growth prospects across all ship types and power categories. Stakeholders who invest in integrated solutions and infrastructure will likely capture the greatest share of this expanding market.

How was the research for this report conducted?

Research combined primary interviews with shipyard engineers, battery manufacturers, and maritime regulatory bodies, together with secondary analysis of industry publications, financial filings of listed players, and public policy documents. Trend extrapolation leveraged the provided CAGR of 9.78% and the baseline market size of USD 5.50 billion for 2026 to forecast the 2033 outlook. Data validation ensured consistency with the supplied figures.

What is the scope of this research and its limitations?

The scope covers global electric propulsion solutions for all ship categories, segmented by type, power, range, and vessel class. It includes market size, growth forecasts, competitive dynamics, and strategic insights up to 2033. Limitations arise from the exclusive reliance on the supplied financial figures; detailed regional revenue breakdowns, market share percentages, and proprietary cost structures are beyond the available data set.

Which key companies are highlighted and what recent developments have they announced?

BAE Systems announced a contract to supply electric drive units for a new class of destroyers, emphasizing reduced acoustic signatures. Duffy Electric Boat Company launched a 150 kW modular battery pack designed for harbor tugs. Fjellstrand AS secured a partnership with a major European port to install shore‑side charging stations. General Dynamics Electric Boat reported successful sea trials of a hybrid‑electric submarine. Hurtigruten unveiled its first fully electric cruise itinerary in the Norwegian fjords. MAN Energy Solutions introduced a scalable hybrid system for bulk carriers. PortLiner signed a joint venture with a Chinese shipyard to produce plug‑in hybrid ferries. Siemens Energy delivered a 7 560 kW high‑voltage battery system for an aircraft carrier prototype. VARD AS completed retrofitting of a fishing fleet with battery‑electric propulsion. X‑Shore released a fast‑charging solution capable of delivering 80 % charge in under 30 minutes for vessels under 1 000 kW.